Save

Save Print

PrintThis week, the volume of ferrosilicon Futures fluctuated upward, which led to the improvement of the transactions, and the spot price continued to rise, with a firm operation; The price of semi-coke on the cost side increased, which also supported the market (It was reported that Shenmu Semi-coke Group has issued a notice: due to the impact of epidemic situation, coal storage in winter, safety and environmental protection and other comprehensive factors, decided to implement the ex-factory tax price of 2000 yuan per ton for large-sized materials, 1900 yuan per ton for medium-sized materials, and 1850 yuan per ton for small-sized materials from 0:00 on September 20); With the National Day holiday approaching, the demand from steel mills to stock up was expected to improve, and the transportation costs in some relevant production areas moved up, market sentiment has improved, confidence has increased, the speed of production recovery in the production areas has gradually accelerated, and the operating rate has rebounded. In the short term, the ferrosilicon market may maintain a stable and strong trend. It was still necessary to pay attention to the Futures market trend and changes in supply and demand relations.

In the downstream, the supply of steel continued to pick up in the traditional peak season, but the release of demand was still less than expected, leading to an increase in the market stock in the peak season. According to the data of CISA, in the middle of September 2022, the key iron and steel enterprises produced a total of 21.4503 million tons of crude steel, with a daily output of 2.145 million tons, an increase of 2.23% month on month; The steel inventory of iron and steel enterprises was 17.661 million tons, an increase of 596500 tons or 3.5% over the previous ten days; An increase of 1.718 million tons or 10.78% over the end of last month; It increased by 331800 tons or 1.91% over the same ten day period of last month; It increased by 6.3641 million tons or 56.34% over the beginning of the year; An increase of 4.3586 million tons or 32.77% over the same period last year. According to statistics, many places released plans to support the construction of major infrastructure projects, and short-term steel prices or shocks were expected to be relatively strong.

For magnesium metal, the price of magnesium was restrained due to insufficient demand in the early part of this week; Since Wednesday, downstream procurement has been followed up, and the price of magnesium has risen steadily. With the National Day holiday approaching, downstream users increased the number of goods to be stocked and replenished, and the transaction situation was heating up; In addition, the prices of coal and ferrosilicon at the raw material end were firm, supporting the high level operation of magnesium price. Under various favorable factors, the short-term magnesium ingot market was expected to be stable. On Friday, the mainstream ex-factory cash quotation including tax of 99.9% magnesium ingots was about 24500-24700 yuan per ton.

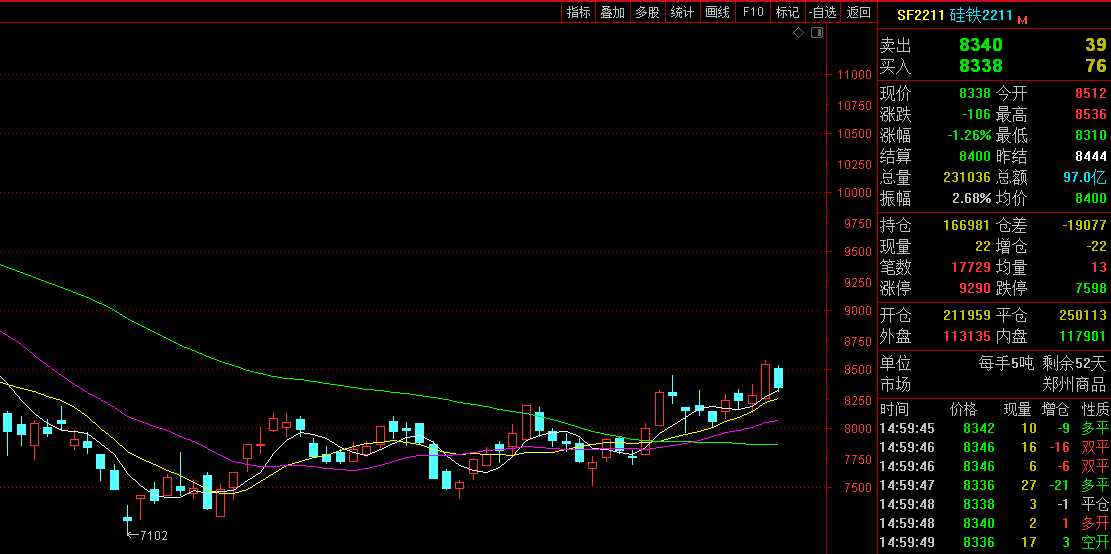

The weekly opening price of 2211 main contract was 8,150, the highest price was 8,586, the lowest price was 8,080, the closing price was 8,338, the settlement price was 8,400, the trading volume was 1,070,702, and the position was 166,981, up 3.60%.

Below are ferrosilicon Futures main contract daily specific performances:

|

Date |

Opening price |

Highest price |

Lowest price |

Closing price |

Settlement price |

Trading volume |

Positions |

Range |

|

9.19 |

8150 |

8300 |

8080 |

8236 |

8220 |

200584 |

167928 |

2.34% |

|

9.20 |

8296 |

8334 |

8154 |

8230 |

8260 |

189910 |

164878 |

0.12% |

|

9.21 |

8212 |

8382 |

8132 |

8284 |

8258 |

199122 |

163344 |

0.29% |

|

9.22 |

8258 |

8586 |

8230 |

8540 |

8444 |

250050 |

186058 |

3.41% |

|

9.23 |

8512 |

8536 |

8310 |

8338 |

8400 |

231036 |

166981 |

-1.26% |

- [Editor:kangmingfei]

Daily News

Daily News Research

Research Magazine

Magazine Company Database

Company Database Customized Database

Customized Database Conferences

Conferences Advertisement

Advertisement Trade

Trade

.jpg)

Online inquiry

Online inquiry Contact

Contact

Tell Us What You Think