Save

Save Print

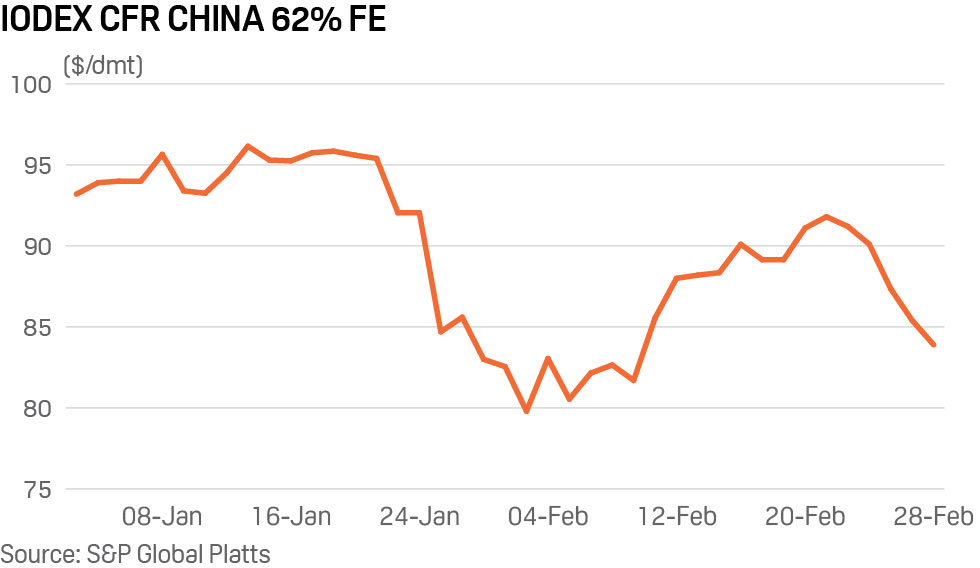

Print[Ferro-Alloys.com] Iron ore prices have fallen 8.6% over the past five trading sessions despite supply tightening due weather events crimping exports from key exporters Australia and Brazil, latest data showed Monday.

S&P Global Platts assessed the 62% Fe IODEX down $7.90/dmt week on week at $83.90/dmt CFR China Friday as expectations faded for a recovery in downstream steel demand in the second quarter while the coronavirus outbreak continues to spread beyond China.

Prices fell sharply despite supply tightening due to a heavy monsoon season in Brazil since December and recent cyclones in Western Australia. Iron ore exports from Brazil averaged 5.22 million mt/week in the first eight weeks of 2020, down sharply from 7.2 million mt/week a year earlier. From Australia, exports averaged 15.76 million mt/week, down from 16.37 million mt/week in the same 8-week period of 2019.

However, market participants expected said the decline in exports to have a limited impact given the weakness in steel demand and expectations that end-users in China would lower production levels or even idle some capacity.

For several weeks after the Lunar New Year, iron ore prices remained largely supported, despite the impact of the coronavirus outbreak in China, as many end-users opted to maintain production and procurement levels.

While smaller and more flexible end-users quickly adjusted their sinter feed to cheaper alternatives or lowered production as steel margins turned negative, large end-users could not follow suit due to the more complicated nature of running large blast furnaces. A decision to lower production rates or adjust their sinter feed would hinge on a longer-term outlook as alterations to their blast furnace production processes are not easily reversible.

However, with accumulating steel inventory levels now affecting storage space, market expectations are for large end-users to begin lowering their production rates in Q2, or to start unscheduled maintenance periods to manage their production costs.

LOW PORT STOCKS SHRUGGED OFF

End-user procurement preferences have been largely in favor of the portside market to date in 2020, which offers more flexibility in volume than securing seaborne cargoes.

But even with iron ore port inventory levels falling to 121.7 million mt last Friday from 125.5 million mt on February 7, market participants remain largely unconcerned.

Port inventory levels are currently not too far off the 114 million-115 million mt level reached in June-July last year that sparked a buying frenzy for seaborne cargoes, but end-user demand this time is weak, an international trader said.

However, despite expectations the impact of tightening supply would be limited on waning end-user demand, a certain level of inflexible demand for some products was expected to support their premium levels.

While negative steel margins generally encourage end-users to adopt cheaper sinter feed fines, end-users are only able to replace a certain percentage of the sinter feed blend.

Weather disruptions have impacted the spot supply of some products and there are end-users who have paid high premiums for prompt-loading cargoes out of necessity, several traders said.

PREMIUM HOLDS FOR KEY GRADE

Market sources expected premiums for low alumina products to be supported in spite of current margins due to lower Brazilian export volumes and the coking costs associated with allowing blast furnace feedstock alumina levels to go above normal tolerance levels.

The delayed restart of China’s domestic low alumina concentrate production after extended Lunar New Year holidays has magnified the impact of lower Brazil’s iron ore exports, which are generally low in alumina.

Export and shipment data seen by Platts showed discharge volumes at Teluk Rubiah from Brazil at 0.8 million mt in January and 1.2 million mt in February as of February 25. This is down sharply from 1.95 million mt in December and 2.3 million mt in January 2019.

Brazilian Blend fines or BRBF produced in Teluk Rubiah in Malaysia are a key ingredient in the sinter feed blend of mills in south China and market sources expected premiums to be supported on account of the suppressed volumes and the mills’ geographical distance from iron ore mines in China’s north.

The other medium grade Brazilian substitutes for BRBF are not as ideal in terms of sintering quality due to sizing differences and, as such, any available spot BRBF cargoes are likely to remain in high demand, several traders said.

Source: Platts

- [Editor:tianyawei]

Daily News

Daily News Research

Research Magazine

Magazine Company Database

Company Database Customized Database

Customized Database Conferences

Conferences Advertisement

Advertisement Trade

Trade

.jpg)

Online inquiry

Online inquiry Contact

Contact

Tell Us What You Think